If you’ve ever worked in the retirement benefits space, you know that keeping track of information between systems is one of the most challenging aspects of managing 401(k) plans, especially if you’re using manual methods to collect and process payroll data. SECURE Act 2.0, which went into effect this year, has upped the ante even further and contributed to the rising popularity of automated 401(k) payroll integrations.

In this article, we’ll cover how 401(k) payroll integrations work, the differences between 180° and 360° payroll integrations, the cost and risks of sharing data manually, and some frequently asked questions.

We’ll also discuss how Finch is powering 401(k) payroll integrations for top players in the retirement benefits industry such as Ameritas, Betterment, and Ubiquity, helping them offer best-in-class 401(k) experiences for employers and employees alike.

How 401(k) payroll integrations work

Most employers, or plan sponsors, outsource the day-to-day work of administering a plan — like enrolling new participants, calculating contributions, and recording deduction amounts — to recordkeepers and third-party administrators (TPAs).

But there’s often still a surprising amount of manual work left to sponsors, even once the plan is in place. Typically, employers must track newly eligible and terminated employees (so they can be enrolled or removed from the plan) and manually update deductions in the payroll system every time an employee changes their contribution amount.

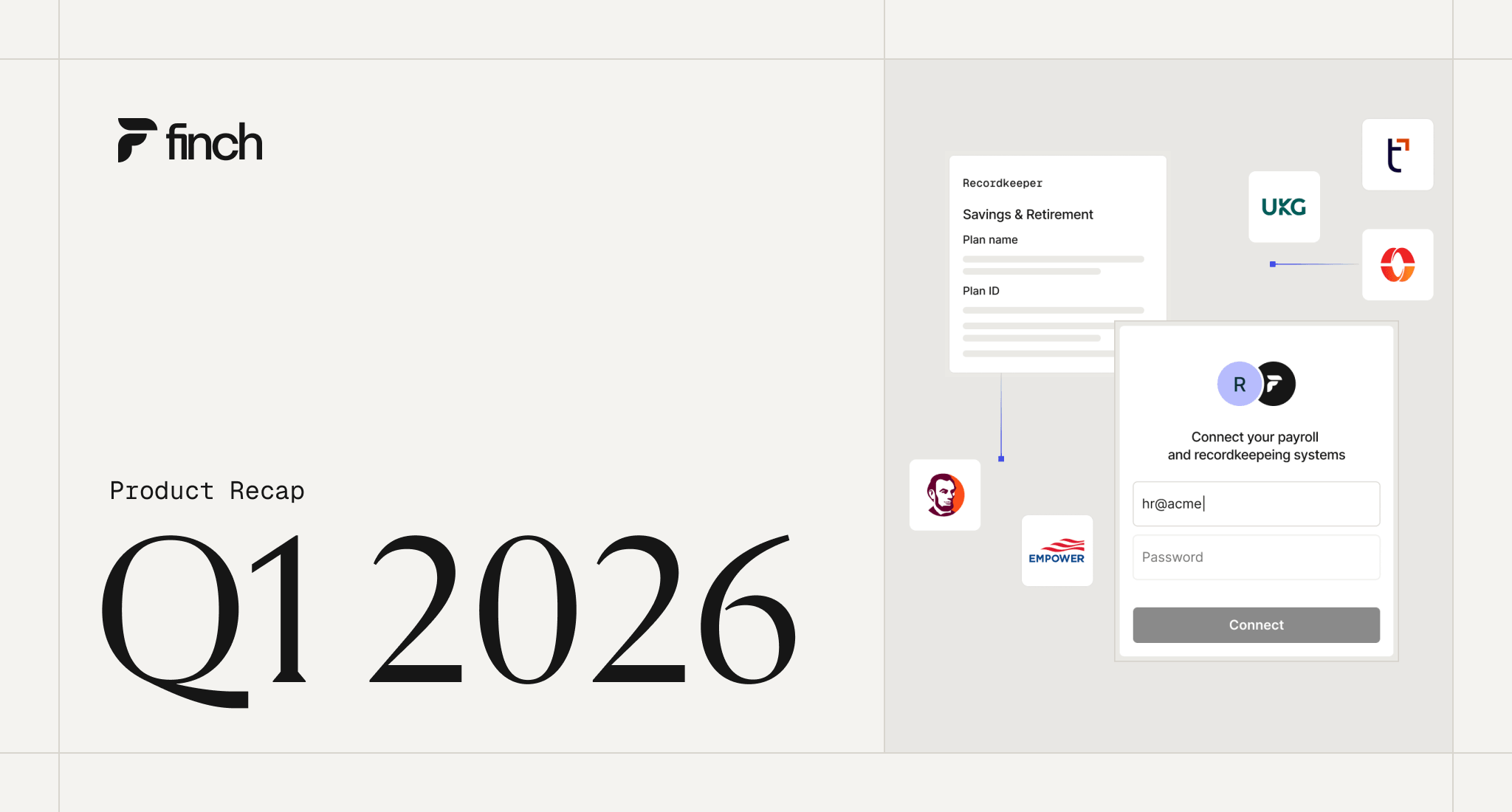

401(k) payroll integrations eliminate this burden for employers by providing a direct connection between the sponsor’s payroll system and their recordkeeper or TPA. As information is updated in the payroll system, such as when a new employee joins the company, that data is automatically relayed to the plan provider. Similarly, as employees make updates to their contributions in the recordkeeper’s platform, that data can be automatically written back to the payroll system.

This automatic flow of data allows recordkeepers and TPAs to pull timely, accurate census and pay information straight from the source in a secure, automated way, while also removing the burden of manually updating eligibility status and deductions amounts from the plan sponsor.

Who benefits from 401(k) payroll integrations?

401(k) payroll integrations are critical to all stakeholders involved in enabling retirement benefits, including plan sponsors, recordkeepers, TPAs, and even payroll providers.

Plan sponsors

401(k) plan sponsors benefit greatly from payroll integrations. They can automate employee enrollment as well as contribution and match updates. This boosts operational efficiency, reduces data entry errors, and eliminates the need for sponsors to manually check and match data.

Recordkeepers

Recordkeepers can harness bi-directional data synchronization — that is, the ability to read employment information from payroll systems and write contribution data back — to reduce data reconciliation efforts and demonstrate higher responsiveness throughout the retirement plan cycle.

In practice, this means that recordkeepers automatically receive updated data as employees join or leave the company, or as they age into different eligibility statuses like those that allow for catch-up contributions. That ensures that the recordkeeper can automatically enroll or un-enroll these employees from the plan. The recordkeepers can also automate deductions management by writing changes to employees’ deductions back to the payroll system without involving the employer, and can monitor other changes — such as an increase in annual salary — to ensure the appropriate amount is being deducted from their paycheck without exceeding IRS contribution limits.

This is more relevant than ever in 2025 with SECURE 2.0 automatic enrollment and escalation mandates. 401(k) payroll integrations let recordkeepers automate enrollment and deductions increases so no one slips through the cracks — and so plans stay in compliance.

Third-party administrators (TPAs)

Third-party administrators can use 401(k) payroll integrations to collect census and pay data, including contribution amounts and salary information, directly from the payroll system. This way, TPAs don’t need to ask for the plan sponsors to send their data during reporting season — they can easily pull the year-to-date data needed for filing Form 5500 and maintaining 3(16) compliance at any point throughout the plan year.

By pulling the data directly from the source, TPAs can minimize data errors and eliminate bottlenecks to work more efficiently and service more clients.

Payroll providers

According to a recent survey we ran, today’s employers on average use 6-7 employment systems. As a result, they are always on the lookout for integrated experiences. As retirement benefits gain popularity among employers in the wake of SECURE 2.0, especially small to mid-size businesses (SMBs), the demand for payroll providers that easily integrate with their chosen 401(k) plan administrators will also rise. This makes integrations essential in the payroll tool decision-making process.

180° vs 360° payroll integrations in 401(k)

Payroll integrations are automated connections between employers’ payroll systems and 401(k) plan providers. There are two types of connections available based on the scope of data flow: 180° payroll integrations and 360° payroll integrations.

180° payroll integrations

In a 180° payroll integration, data flows in one direction — from payroll providers to the plan provider’s system. This means whenever employment data (such as termination, address, promotion, etc.) is changed in payroll systems, a 180° integration will automatically update the information in the recordkeeper or TPA’s platform.

However, if an employee modifies their contribution details in the provider's platform, it will not be reflected in the payroll system. The employer will have to update the changes on the payroll platform manually, which leaves room for data entry errors.

360° payroll integrations

With 360° payroll integrations, data moves in two directions — both to and from the payroll system and the plan provider’s platform:

- Any data updated in the payroll system is synced with the provider’s system.

- Any contribution changes made in the recordkeeper’s platform are automatically adjusted in the payroll system.

This ensures consistent and up-to-date information exchange between all systems of record. Recordkeepers can automate the entire benefits workflow, from enrollment to deductions changes. For this reason, 360° payroll integrations are often favored by sponsors and administrators.

Benefits of 180° and 360° payroll integrations

A complete integration between payroll and 401(k) systems is critical as recordkeepers and TPA seek to serve more clients without scaling their internal teams. Integration solves multiple problems for the retirement benefits ecosystem.

Reduce administrative burden and save time for plan sponsors

Extracting and uploading data manually from one system to another every pay period is inefficient and a waste of valuable time. Employers can save significant time by using integration technology to automatically track, and capture, and share retirement data changes with their plan provider.

Improve data accuracy to maintain compliance

Retirement is a heavily regulated industry with strict compliance requirements that depend on both accurate data and timely updates.

The manual data entry process is prone to errors, presenting a risk to compliance. Waiting for sponsors to share fresh data can also cause delays in submitting annual reports or updating deferral details, leading to late investments, penalties, and increased tax liability for employers and employees.

401(k) payroll integrations automate and eliminate compliance risks by directly capturing data from the employer’s source of truth automatically or on-demand.

Improve 401(k) yearly testing and reporting with streamlined data collection

Since 401(k) plans are subject to annual tests and reports to maintain compliance, TPAs have to request full plan-year data from the employer at least once annually. As 3(16) fiduciaries, TPAs and recordkeepers may want to review this data multiple times throughout the plan year to ensure they’re in compliance, or to warn sponsors whose plans are at risk of failing nondiscrimination tests or other regulatory requirements.

But collecting this data can be a challenge, especially because most plan sponsors are not fully aware of all the data necessary for these annual tests and reports. TPAs often need to request files from sponsors multiple times because fields are missing or because they simply forgot to send the data.

180° or 360° payroll integrations allow TPAs and recordkeepers to automatically collect census and pay data — including contribution amounts, salary information, demographic data, birth dates, hire dates, and more — so testing and reporting can be streamlined and much more efficient.

Read more: How to Streamline 401(k) Compliance Testing with Payroll Integrations

Enhance the sponsor experience

As a 401(k) plan administrator, your ability to attract and retain clients depends on two things:

- How much administrative burden you can reduce for them

- How easily they can navigate between different systems they already use

Payroll integrations allow you to do both so you can deliver a straightforward, easy-to-use, automated plan experience. You’ll be able to spend more time advising sponsors and less time collecting and processing employer data.

Read more: How to Improve 401(k) Plan Sponsor and Participant Experience

Ready to automate with 401(k) payroll integrations? Let Finch help

Finch powers payroll integrations for more than 40 leading retirement providers, including Ameritas, ePlan (Paychex), Betterment, and Ubiquity with support for 50+ payroll providers covering 80% of all US employers. Want to learn more? Set up a call with our Sales team today.

FAQs about 401(k) payroll integrations

1. What is the best payroll integration method?

Most 401(k) administrators prefer a 360° payroll integration because it enables them to both read data from the payroll system and update contribution changes. Plus, it saves their clients the headache of manual data entry.

But a 180° payroll integration is better than no integration. Plus, only some payroll systems support 360° integrations.

Regardless of the use case, manual data entry is the least preferred method for most sponsors and providers due to its inefficient and outdated mechanisms.

2. How much do payroll integrations cost?

The cost of implementing payroll integrations depends on whether you build them in house or outsource to a connectivity provider like Finch.

Building integrations in house requires technical expertise and hundreds of hours spent building, testing, deploying, and maintaining the connection. By our estimate, building just one payroll integration can cost retirement providers upwards of $187k. Now, multiply that by the 660+ payroll software systems in the US, and you’ll see how challenging this can be.

By contrast, you can work with a provider like Finch to unlock access to a multitude of payroll systems through a single integration, outsourcing the work of building and maintaining integrations and saving significant costs.

3. What is the best way to implement a 360° payroll integration strategy?

If you’re a recordkeeper or TPA, create a shortlist of payroll providers that your customers use most. Then explore what a direct integration might look like for each — or contact Finch.

Finch is an end-to-end connectivity platform for HR and payroll that makes payroll integrations quick and easy to implement. It allows applications to read accurate employment data and write back deduction details back into the payroll system.

No manual data entry, bulk upload, or SFTP setup is needed. Learn more about Finch’s automated deductions.

How is Finch different from other payroll integration solutions on the market?

- Largest payroll network: Finch has the largest network of supported payroll providers on the market, with support for 50+ providers covering 80% of all US employers.

- Streamlined employer onboarding: Using our built-in onboarding tool Finch Connect, sponsors can connect their payroll to your platform in minutes.

- Outsourced integration management: Finch manages the ongoing maintenance of our integrations so you don’t have to.