Since its debut in 1978, the 401(k) plan has become a prized perk for big corporations to attract top talent. However, the steep setup and upkeep costs, administrative issues, and the lack of suitable small business retirement plans have since limited small and mid-sized business (SMB) employers’ ability to offer such plans. Today, while more than 90% of employers with 500+ employees offer a 401(k), the opposite holds true for those with fewer than 100 employees. Only a third of these companies offer their employees a 401(k) option.

Fortunately, the tides are turning. Recent legislative updates like SECURE 1.0 and 2.0 introduced several initiatives for SMB sponsors like Pooled Employer Plans (PEPs) and start-up tax credits. This sparked a wave of new SMB employers entering the retirement market, increasing the demand for personalized small business retirement plans.

While the influx of new sponsors is a positive development for retirement service providers like recordkeepers, third-party administrators (TPAs), and plan advisors, it also presents its own challenges. SMB sponsors often need extra support and watch their costs closely. Managing numerous small business retirement plans also adds to the workload of recordkeepers.

To succeed in this changing landscape, recordkeepers need to find innovative solutions and build efficient automated workflows to handle the increasing demands while maintaining profitability and steady growth. In this article, we'll explore the challenges of serving first-time SMB sponsors as a retirement service provider and how recordkeepers can serve them efficiently.

Common challenges of serving new, first-time SMB 401(k) sponsors

To reduce the coverage gap and manage small business retirement plans better, it’s crucial for recordkeepers and TPAs to understand what makes some small firms offer a 401(k) plan while others don’t. This involves considering factors like revenue stability, business size, 401(k) plan costs, and how much administrative work it takes to manage the plans.

Managing 401(k) plans for new small and medium-sized business (SMB) sponsors poses several challenges for recordkeepers, including:

- SMB sponsor’s limited awareness of retirement plans and available incentives

- Increased need for ongoing customer support

- Cost sensitivity among SMB sponsors

- Higher demand for customization

- Difficulty accessing data from SMB payroll systems

- Increasing operational workload with more SMB clients

Challenge 1: SMB sponsors lack awareness of retirement plans and available incentives

Many small firms aren't familiar with the range of retirement plan options available to ease their cost and administrative burdens. While most know about 401(k)s, few are acquainted with SIMPLE, SEP, and MEP/PEP plans, and 72% reported being unaware of tax credits that could help offset the startup costs of launching a new plan. They also tend to overestimate the financial and time commitments needed to offer a plan.

Lack of awareness and misconceptions about retirement plans make SMB employers hesitant to start their own retirement plans. Although SECURE 2.0 aims to increase the number of SMB employers offering 401(k) plans, recordkeepers will need to put in significant effort to overcome the inertia in the untapped SMB market.

Challenge 2: SMB sponsors need more ongoing customer support

SMB sponsors often lack the know-how and resources needed to effectively support a retirement plan. From selecting the right plan to handling ongoing management, the prospect of starting a plan can overwhelm already busy business owners and small HR teams. In fact, 63% of SMB employers not offering retirement plans cite resource constraints as the reason.

Under this scenario, recordkeepers stepping in to assist small businesses must simplify routine activities like plan enrollment, compliance testing, contribution investment, and deduction management. They should also provide ongoing support to help sponsors navigate the complexities of 401(k) plans and stay abreast of regulatory changes with the necessary resources.

Challenge 3: SMB sponsors are cost-sensitive

Small businesses are usually hyper-focused on costs. A lot of owners and HR managers assume that traditional retirement plans are too pricey and involve additional fees and hidden costs. In fact, about half of small businesses with 99 or fewer employees say they find it hard to afford retirement plans. Their cost sensitivity is further amplified due to the volatile cash flow of small businesses.

Recordkeepers aiming to help them out need to support modern plan options like PEPs to help new sponsors cut down administrative costs of setting up a plan. They also need to figure out better pricing models, innovative solutions, and operational strategies that balance making a profit with offering competitive rates and top-notch services.

Challenge 4: SMB sponsors need greater customization

Similar to big companies, small and mid-sized businesses (SMBs) have diverse employee demographics with varied financial goals. This leads SMB employers to seek personalized retirement plans akin to larger organizations. However, because of limited resources and budget constraints, achieving enterprise-level customization is often challenging for them.

To win more SMB businesses, recordkeepers need to tailor their services to suit these diverse needs and preferences. They need to adopt ingenious approaches, flexible systems, and automated processes that can accommodate a wide range of unique client needs at a lower cost.

Challenge 5: Difficulty accessing data from SMB payroll systems

As a whole, the retirement industry is still heavily reliant on outdated data-sharing methods for accessing sponsor payroll data. Currently, the most common method recordkeepers use is SFTP, which is manual and inflexible, like any file-based data-sharing method. This hands-on method adds more stress to sponsors who already lack the bandwidth to manage a plan. With SFTP, sponsors often need to routinely create, update, and share data files with recordkeepers to keep everything running smoothly.

On top of that, setting up SFTP connections is time-consuming and resource-intensive, which further burdens recordkeepers with manual tasks and extensive back-and-forth communication.

In this scenario, automated solutions like API integrations can be a superior alternative for recordkeepers to seamlessly access sponsor data from their payroll systems. However, the SMB payroll market in the U.S. is highly fragmented, with nearly 6,000 payroll providers, and only a few of them allow other applications to integrate directly. In fact, the vast majority of payroll providers either have a gated API or no API at all—adding to the pain of accessing payroll data.

Challenge 6: More SMB sponsors means a greater operational burden

With more SMB employers offering retirement benefits, the daily workload for recordkeepers’ Operations, Engineering, and Client Success teams is set to skyrocket. Balancing this surge in workload while maintaining service quality becomes paramount for recordkeepers striving to meet their clients' needs effectively. The current industry norm relies heavily on manual processes, from validating sponsor data to managing fund investments—adding friction to each step of plan administration. This leaves recordkeepers facing a crucial decision: substantially grow their Operations headcount or seek more efficient solutions.

How 401(k) recordkeepers can streamline small business retirement plan management

To enhance their service delivery and better meet the needs of SMB sponsors, recordkeepers can take several steps. They can:

- Automate processes to improve operational efficiency

- Simplify data access to develop smoother and faster workflows

- Leverage modern technology to offer best-in-class customer support

Automate processes to improve operational efficiency

First and foremost, to effectively handle the growing workload, recordkeepers should prioritize automating tasks that are currently done manually: automatically enrolling employees based on eligibility, quickly determining what dollar amount to invest, and pushing changes directly back to the payroll system. This allows recordkeepers to reallocate Operations headcount to other teams and invest more resources into strategic initiatives like attracting new customers and improving their product offerings. Read our latest whitepaper to delve deeper into how recordkeepers can streamline the processes involved in managing 401(k) plans through automation.

Simplify data access

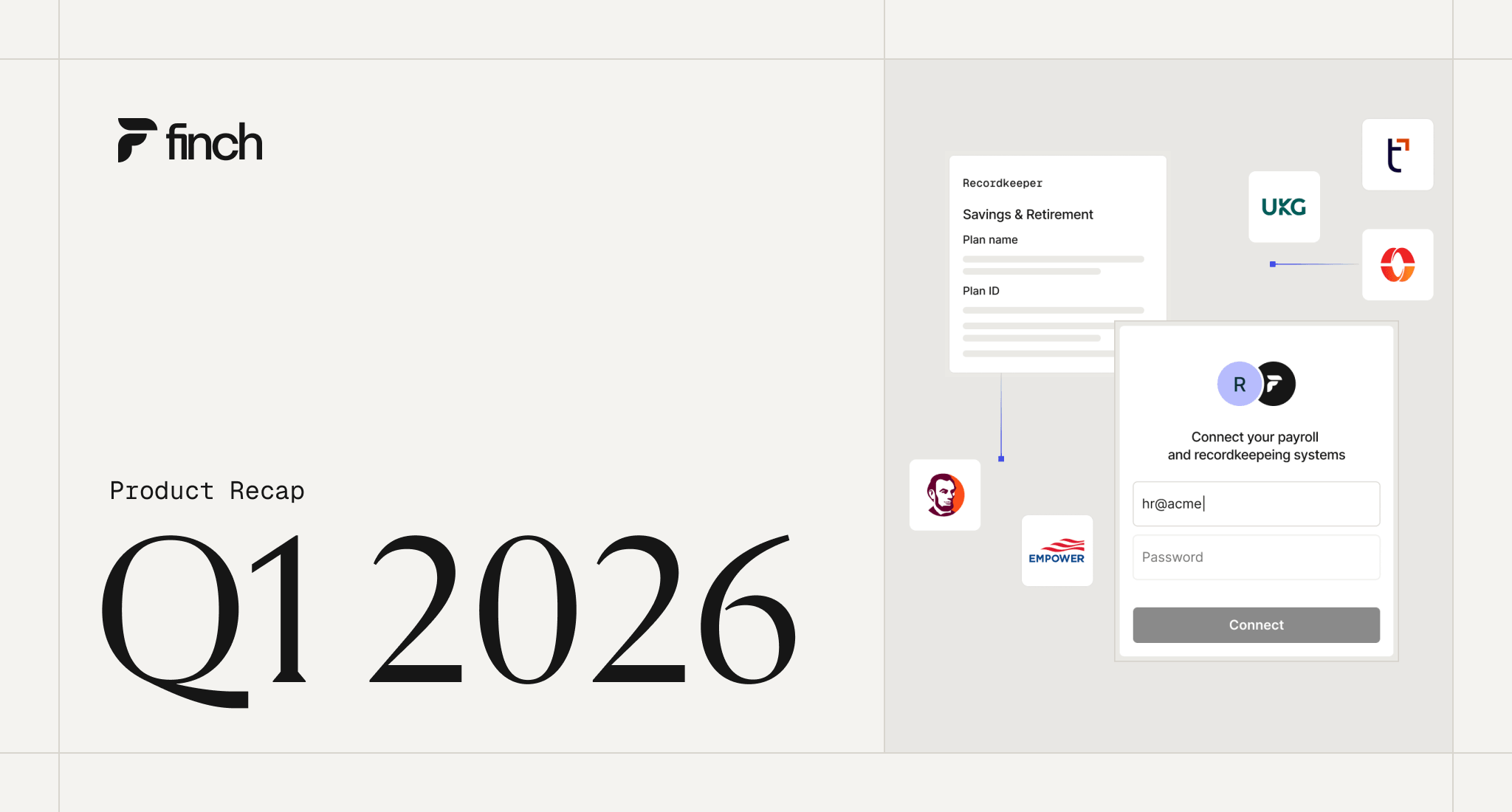

Much of the manual labor involved in managing 401(k) plans revolves around creating and sharing data files with each pay period. To truly automate plan management, it's crucial to leverage innovative solutions that streamline data access. Recordkeepers can greatly benefit from using integration tools like unified APIs, which offer quick and reliable access to multiple payroll systems through a single integration.

Unified APIs also standardize data from various providers into a common format, making it easier to work with. Take Finch’s Unified API for instance, which integrates with multiple payroll providers, including niche, long-tail platforms tailored to serve small and mid-sized businesses. Automated integrations enable recordkeepers to automatically fetch income and deferral rates each pay cycle and seamlessly update deduction changes back to the payroll system without involving the sponsor—while significantly reducing engineering costs. Such efficiency greatly eases the burden on the recordkeeper’s Operations team and ensures a smooth user experience.

Offer best-in-class customer-support

As mentioned earlier, many SMB sponsors don’t offer retirement plans because they aren’t familiar with the available options, incentives, and fiduciary responsibilities. Recordkeepers who can offer a better user experience, simplify plan setup and management, and reduce the administrative burden of already overworked HR teams will emerge as the most employer-friendly solutions and win the long game of customer retention and loyalty in an increasingly competitive U.S. retirement market.

Unlock access to hundreds of payroll and HRIS systems with Finch

Finch’s Unified Employment API streamlines operations for retirement and benefits providers by eliminating the need for manual data processing. It helps you spend less time building technical bridges and more time tailoring your product and services to better serve SMB sponsors. With access to over 200 payroll and HRIS systems powered through a single integration, Finch offers the widest and deepest coverage available—4x more than any other unified API. Schedule a call with our sales team to learn more, or try it yourself for free.