For recordkeepers and TPAs, handling annual 401(k) compliance testing is like steering through a maze of IRS and DOL rules. As stewards of these plans, they need to keep up with regulatory changes, employee census updates, and payroll deductions and accurately process large volumes of participant data without missing critical deadlines.

This is as complex as it sounds, particularly when accessing employee data isn’t straightforward. Think of it like juggling multiple balls—you've got to be on your game to keep all the balls in the air and avoid any penalties along the way. The challenge is further amplified for plans with complex designs, like profit sharing or multiple investment options. As if that weren’t enough, recordkeepers and TPAs have to deal with the frustration of slow and error-prone manual data sharing methods.

Traditional ways of handling employment data have long proved to be a hassle for plan service providers that slows down the efficiency of plan management including compliance testing. This has prompted recordkeepers and TPAs to actively seek new technologies, leading to the recent popularity of API-based payroll integrations.

APIs provide TPAs and recordkeepers with direct and immediate access to sponsors' payroll data. This not only simplifies compliance testing but also minimizes sponsor involvement in retirement plan management—enabling them to create a winning customer experience.

In this article, we’ll explore the concept of compliance testing, the limitations of traditional data sharing methods for effective testing, and how recordkeepers and TPAs can leverage payroll integrations to streamline the testing process.

Understanding 401(k) compliance testing

Sponsors have a fiduciary responsibility to guarantee fair and equitable benefits for all participants in the 401k plan. Each plan must pass four key compliance tests to ensure the plan doesn't favor higher-income individuals like business owners and top executives. The four tests are:

- Coverage test

- Actual Deferral Percentage (ADP) test

- Actual Contribution Percentage (ACP) test

- Top-heavy tests

The coverage and nondiscrimination tests (ADP and ACP) are annual assessments focused solely on contributions made within a specific year, while the top-heavy rules are evaluations based on the cumulative benefits accrued over time.

- Coverage testing ensures that a broad spectrum of employees benefit from the plan. It verifies that the retirement plan sufficiently covers non-highly compensated employees (NHCEs) in comparison to highly compensated employees (HCEs) and key employees. For plan administrators, this involves accurately assessing whether NHCEs are adequately included in 401(k) plans.

- Actual Deferral Percentage (ADP) testing checks if HCEs contribute within defined limits relative to NHCEs.

- Actual Contribution Percentage (ACP) testing evaluates employer-matching contributions and voluntary after-tax contributions. The purpose of the ACP test is to confirm that the plan feature is actually used widely and not only by HCEs.

- Top-heavy testing confirms that plans do not excessively favor key employees. Plan administrators must keep an eye on the plan’s overall structure to verify that the plan benefits all employees proportionally.

All plan sponsors are obligated to complete compliance testing unless their plan qualifies for the Safe Harbor exception. The success of a 401(k) plan in these tests hinges on the spread between compared groups falling within the specified range. If a significant discrepancy is detected, the employer must take corrective actions as outlined by the IRS in the 401(k) Plan Fix-It Guide.

Common 401(k) compliance testing challenges

For third-party plan administrators and recordkeepers, compliance testing involves deep analysis and meticulous scrutiny of the plan and participant data. Delays or errors in these calculations can result in hefty penalties and additional matching requirements for plan sponsors. If you’re a recordkeeper or TPA, this is definitely not the sponsor experience you’d want to create for your customers.

Ensuring the data is accurate and received on time is a considerable challenge for recordkeepers and TPAs, primarily because they’ve traditionally been reliant on the sponsors or their payroll providers to send the data manually or through file-sharing methods like SFTP.

Exchanging data this way can present a slew of challenges, like:

- Outdated employee details

- Incorrect employment data

- Lack of standardization across systems

Outdated employee details

Manual methods like SFTP can cause unnecessary delays in accessing required data. By the time a file is uploaded on the server, it’s theoretically out of date. Any changes that are made in the payroll system in between data dumps (which typically happen once following each pay period) are unknown to the recordkeeper or TPA until they receive the next batch of data. This delay may result in TPAs and recordkeepers missing important eligibility information or deferral updates and miscalculating the participation rate and contribution percentages of HCEs, NHCEs, and key employees, leading to inaccurate reporting.

Incorrect employment data

SFTP and other file-based systems often require ongoing manual intervention: if the sponsor is in charge of sharing data with the recordkeeper, they need to download data from their payroll system, format it appropriately, then upload that file onto a shared server. That much human intervention creates ample opportunity for errors like typos, mislabeled fields, and improper formatting. Since the quality of 401(k) compliance testing relies on the accuracy of this data, even small inaccuracies can lead to bad test results, resulting in fines, penalties, and extra work to fix mistakes. It also hurts the recordkeeper’s or TPA’s reputation and credibility.

Lacking data standardization

File-based data sharing methods don’t account for the lack of standardization across payroll providers, forcing recordkeepers and TPAs to spend resources extracting and standardizing the data before it can be used in compliance testing. In the diverse U.S. payroll market, where nearly 6,000 providers—each with their own unique data formats and fields—cater to small and mid-sized businesses (SMBs), standardization is key. This complexity leaves further room for error and draws out the testing process, risking missed deadlines.

Simply put, ensuring data quality and consistency can be challenging, time-intensive, and inefficient, especially when working with a year’s worth of sponsor data. Recordkeepers and TPAs need a better way of collecting this data at compliance testing time. This drives them to seek out more automated solutions like API integrations.

How API integrations improve 401(k) compliance testing

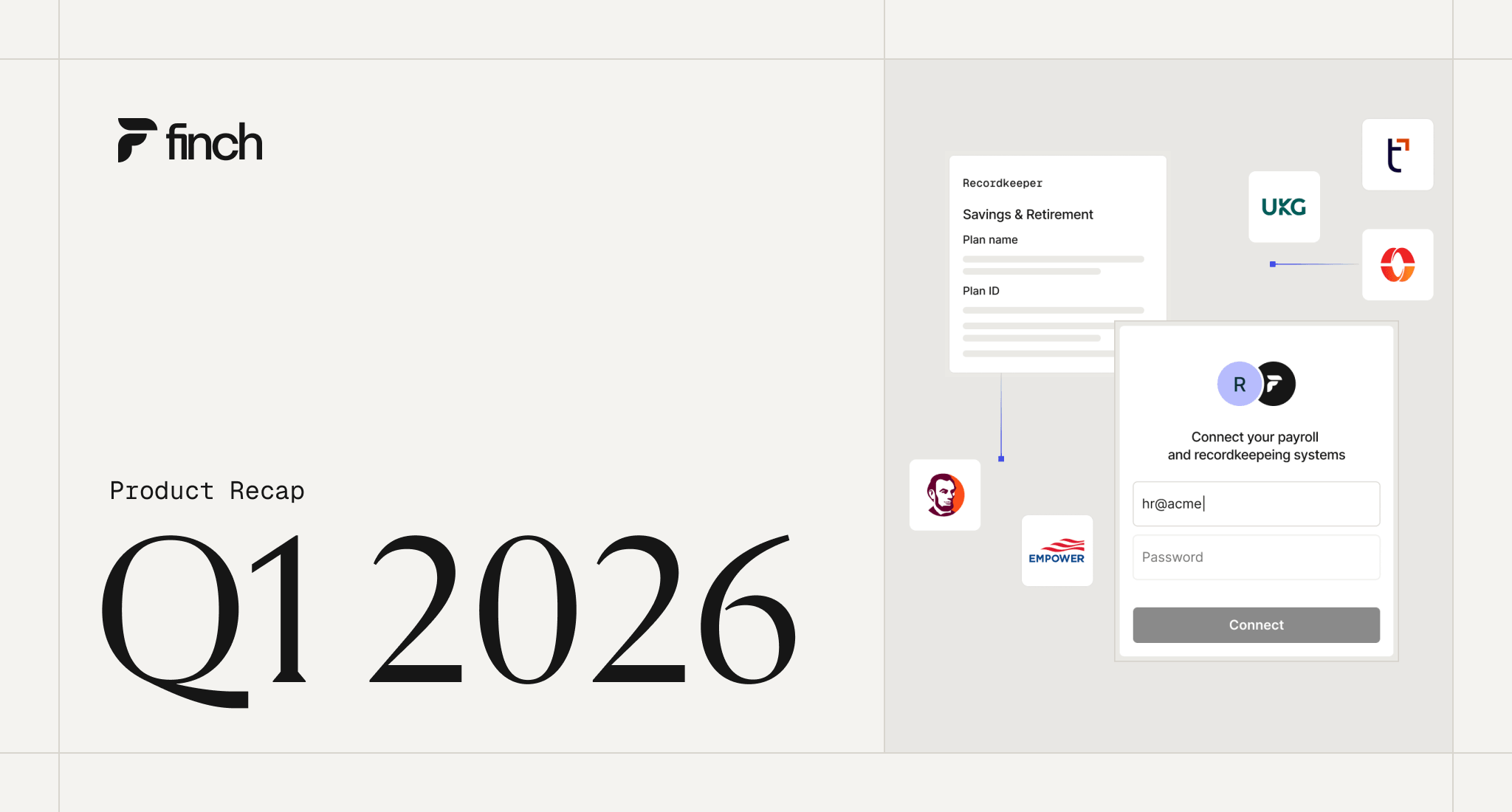

Application programming interfaces, or APIs, are tools that allow software applications to communicate and interact with each other. With API-based payroll integrations, data can automatically flow from the sponsor’s sources of truth directly to the recordkeeper or TPA—for each pay run.

There are two types of payroll integrations: 180° and 360°. While 180° integrations only transmit data in one direction—say, from the payroll system to the recordkeeper—360° integrations facilitate data exchange in both directions. This means recordkeepers can update deductions directly in the payroll system without involving the sponsor.

360° payroll integrations offer several advantages in compliance testing. It helps recordkeepers and TPAs to:

- Seamlessly sync employee census data throughout the year

- Keep track of employee deferrals

- Collect YTD data for end-of-year audits

- Improve the sponsor experience

Seamlessly synchronize employee census data throughout the plan year

Sponsors’ census data is changing all the time. Payroll integrations ensure that the recordkeeper or TPA is always holding the most recent employee information. Whenever employees are on- or off-boarded, receive promotions and raises, or change roles, that information is synced between the payroll system and the recordkeeper and TPA’s database.

This allows them to track HCE and NHCE contributions throughout the year and make necessary adjustments to ensure the plan will pass compliance tests.

Keep track of employee deferrals

In many plans, participants can change deferral rates at any time, which means the recordkeeper has to notify the sponsor so they can make the necessary adjustments within the payroll system. But with 360° integrations, the recordkeeper can automatically push deferral changes back to the payroll system without involving the sponsor at all. This ensures the changes are made before the next payroll and that the recordkeeper has the most up-to-date information regarding the employee’s deferral and potential matching contribution.

Collect YTD data for end-of-year audits

Using API integrations, recordkeepers and TPAs can efficiently retrieve year-to-date (YTD) data from sponsors for end-of-year audits. This allows them to check the accuracy and completeness of data pulled throughout the year and make any necessary adjustments before the year’s end. Accessing YTD data through APIs simplifies 401(k) compliance testing by giving immediate insights into the year-long participant contributions and plan activities, which improves the accuracy of testing and regulatory reporting.

Improve sponsor experience

360° API integrations enable recordkeepers to enhance the sponsor's experience by reducing their day-to-day involvement in 401(k) plan management, minimizing administrative responsibilities, and eliminating constant back-and-forth through automated data transfer. Moreover, more automation leads to higher operational efficiency for the recordkeepers.

Note: For a detailed understanding of how payroll integrations can streamline 401(k) plan administration, including compliance testing, read our article "Why Recordkeepers are Increasingly Turning to Payroll Integrations."

Best practices for streamlining 401(k) compliance testing with 360° API integrations

For a 401(k) plan to pass compliance testing, it must be non-discriminatory and avoid being top-heavy. As a 3(16) fiduciary, recordkeepers and TPAs bear the responsibility of upholding the plan's financial integrity, meeting regulatory standards, and ensuring participants have a secure retirement savings experience. Proactive maintenance and regular updates of plan records mitigate the risk of test failure and eliminate the need for major adjustments at year-end.

To streamline compliance testing, recordkeepers can implement the following strategies that involve maintaining current data, conducting timely testing, and continuously monitoring the plan's performance:

- Use API integrations for seamless and secure data exchange

- Implement automatic enrollment

- Regularly review plan participation and contribution data

- Adopt integration tools to scale payroll integrations

Use API integrations for seamless and secure data exchange between systems

Traditional file-based data sharing methods are manual, error-prone, and may require sponsors to perform routine work. API integrations, on the other hand, allow recordkeepers to access employment data in a fast, secure, and programmable manner—ensuring they always have all the data required for compliance tests.

Implement automatic enrollment to make it easy for employees to join 401(k) plans

With automatic enrollment, eligible employees are enrolled by default, shifting participation from opt-in to opt-out. Payroll integrations keep plan records up to date by enrolling employees as soon as they become eligible and boosting overall NHCE contributions, which increases the likelihood of passing non-discrimination tests (NDTs). Moreover, automatic enrollment helps administrators and sponsors comply with Section 101 of the SECURE Act 2.0 that mandates automatic enrollment in retirement plans.

Regularly review plan participation and contribution data

Recordkeepers and TPAs should regularly review sponsors’ data for accuracy to catch potential issues with the ADP and ACP tests early. While API integrations guarantee that they are receiving the data exactly as it appears in the payroll system, mistakes can still happen—the sponsor may have inadvertently added a typo or input data into the wrong field.

But when recordkeepers and TPAs have access to all of a sponsor’s data—historical and present—at all times, it’s easy to perform routine checks to ensure the data is clean. That way, errors can be caught early and addressed before compliance testing deadlines roll around. They can also warn sponsors if the trend shows skewed contribution ratios at any time throughout the year.

Adopt integration tools for accessibility and scalability

While payroll integrations provide significant value, building and maintaining 1:1 integrations at scale can be challenging and costly. Payroll APIs are typically specific to each provider and may require in-depth knowledge of the application's functionality and API structure. This is why integration tools like unified APIs are gaining popularity among recordkeepers and TPAs.

Unified employment APIs enable them to access data stored in multiple payroll systems through a single integration. Unlike their generalized counterparts, unified employment APIs are hyperfocused on the employment sector, which means they can offer more granular data access. For example, Finch’s Unified Employment API can fetch data as deep as individual pay statements. This level of detail makes it easy to check participant details such as earnings, tax information, and deductions.

It’s safe to say that relying on sponsors to manually share employee demographic, payroll, and plan contribution data over an SFTP server is neither efficient nor scalable for recordkeepers and TPAs that are looking to simplify compliance testing for 401(k) plans. As more employers seek integrated and technology-driven solutions, they are leaning heavily towards payroll integrations to automate critical steps in compliance testing—from automated data access and eligibility checks to boosting plan participation and managing deferral updates.

Simplify 401(k) compliance testing with Finch

Finch’s Unified Employment API can simplify compliance testing for recordkeepers and TPAs in several ways:

- Finch provides secure access to multiple payroll systems—covering 88% of the U.S. employer market—with a single integration. This helps recordkeepers and TPAs to effortlessly scale payroll integrations at a lower engineering cost.

- With direct integrations to the sponsor's system of record, TPAs and recordkeepers can speed up employer onboarding, auto-enroll newly eligible employees, and simplify deductions updates with minimal effort.

- Finch standardizes employment data across providers into a common data model that’s easy to understand and work with.

There’s more to what Finch offers. If you're a retirement plan service provider managing compliance testing for multiple employers, consider adding Finch to your tech stack. Get in touch with us today to see how we can help.